Author, Andrew Gibson

Author, Andrew Gibson

Last Updated on August 2nd, 2024

You can transfer money to the UK from Switzerland using either a bank or a money transfer specialist.

I’ll explain how the process works, how long it takes, the costs, and how to get a better rate.

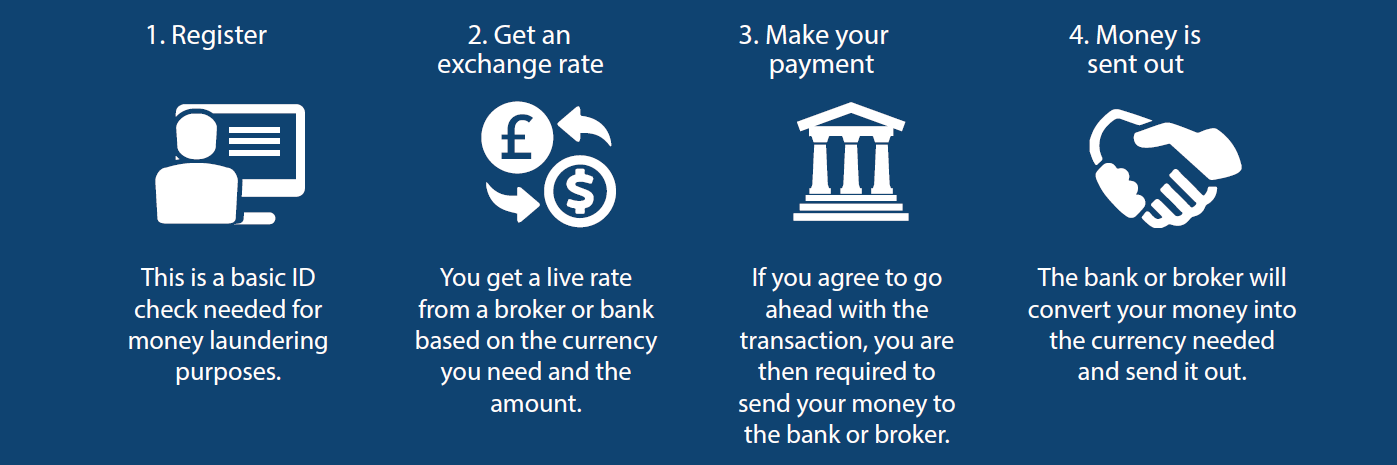

How to transfer money from Switzerland to the UK (in 4 simple steps)

Sending money from Switzerland to a UK bank account is quite straightforward once you understand the process.

Step 1 – Verify your identity

Before you can send money abroad, all customers are required by law to have an identity check.

You will be asked for the standard information – name, date of birth, and address.

Only new customers need to be verified. Once you are set up, you can skip this step in the future.

Step 2 – Secure an exchange rate

Once you are verified, you can secure an exchange rate if you’re ready.

To send money from Switzerland to the UK, it is the Swiss Franc (CHF) to Pound Sterling (GBP) exchange rate that matters to you.

A bank or money transfer specialist will quote you their latest CHF/GBP rate.

You then decide whether to proceed.

No transaction will occur without your authority.

If you are happy to go ahead, the exchange rate quoted is locked-in for you.

You will also be emailed a trade confirmation that shows all the details of your transaction and where to send in your Swiss Francs.

Step 3 – Send in your Swiss Francs

If you are dealing with a regulated company, you will be sending your money to a safeguarded client bank account for Swiss Francs.

In practice, it’s like paying a domestic bill.

Note – a bank will require you to have your CHF in your account upfront, whereas a money transfer company will allow you to secure an exchange rate before you send your money in.

Step 4 – Your Francs are converted to Pounds and sent to the UK

You will also need to provide the details of the UK bank account where you want your funds sent.

Once your bank or money transfer company has received your Swiss Francs, they will be converted into Pounds at the exchange rate agreed.

You will also be asked for some basic information about your recipient’s bank details.

Your Pounds will then be sent to the UK bank account you request.

How long does it take?

In practice, it normally takes 2-3 working days to transfer money from Switzerland to the UK.

You may come across companies claiming they carry out a ‘same-day transfer’.

But that just means they will convert your money and send it out on the same day.

The truth is your UK bank will take a few days to clear the funds into your account.

There’s nothing to worry about (it’s not a tax thing) – but you can’t speed it up.

It’s also a fact of life that some payments clear faster than others.

If you want your money quickly, you can expedite the process by sending your funds beforehand.

That way your money will be ‘outbound’ as soon as possible.

Banks vs money transfer specialists – what’s the difference?

A bank or money transfer specialist can get the job done.

It’s mainly a case of cost and service differences.

Using a bank might be a convenient option for small, regular bills back home.

But if you’ve sold a property or want to repatriate a large sum of money from savings or investments, it’s worth your while looking at the alternatives.

From speaking to many customers over the years, I know that banks aren’t normally the best or cheapest way to transfer money from Switzerland to the UK.

Banks can be frustrating to deal with, and their charges can be high.

The larger the transfer, the more the cost and service differences will become apparent.

Money transfer companies also don’t have any limits on the amount of money you can transfer.

Some money transfer companies also allow you to:

- Fix an exchange rate for an agreed period (usually up to 12 months).

- Set target levels or specific limits for the rate, or

- Inform you when the exchange rate moves in your favour.

Ultimately, these service features can lower your costs and minimise your risk.

Money transfer companies also don’t have any limits on the amount of money you can transfer, whereas banks do.

Banks are not set up to provide anything other than a basic service.

And that service seems to be getting less and less.

| Pros | Cons | Best for | |

| Bank | Can use your existing account | High charges, minimal service | Small payments, convenience |

| Money transfer specialist | Lower cost, more efficient | Need to register | Large or regular amounts |

The charges explained (including the hidden ones)

When you send money from Switzerland to the UK, there are two types of charges you need to look out for:

- Fees

- Exchange rate

1. Fees

It takes a bit of digging to find out the fees the big Swiss banks charge.

They all use their own terminology, and there are a bunch of different payment types to confuse matters further.

Banks generally a flat fee charged for every international transfer.

Below is a quick summary of what the big three in Switzerland charge:

- PostFinance (Post Office) charges a CHF 2 fee online or CHF 5 for a paper-based transfer using Giro International. They also add another CHF 12 for urgent payments.

- Credit Suisse charge CHF 24 for international and foreign currency payment.

- UBS charge CHF 5 for an outgoing online payment or CHF 10 for a paper-based payment.

But there can be other fees too…

I won’t bore you with pages of ‘special tariffs’ (some of these PDFs run for 20 pages!).

Essentially if you want anything extra like an amendment, cancellation, or investigation, you will be charged around CHF 30-60 per request.

It’s also a common problem to get hit with a correspondent or intermediary fee.

This is when another bank assists your bank to facilitate the payment.

If you want to avoid fees, avoid the banks.

2. Exchange Rates

Most of the time the exchange rate you get is more important than the fees.

Every bank and money transfer specialist set their own exchange rates.

The exchange rate will depend on the amount of Swiss Francs you are sending (the more you send, the better the rate).

I’ve looked into the exchange rates offered by PostFinance, Credit Suisse, and UBS.

PostFinance offers a free currency converter, but then has a big fat disclaimer saying “No guarantee of accuracy is given”.

UBS and Credit Suisse provide little information upfront.

The Swiss banks seem to make it difficult to get an exchange rate before you make a transfer.

I suspect what happens is you go through all the steps, get to the end, and then they tell you the rate.

At that point, a lot of people will just accept it – no matter how bad it is.

The UK banks tend to do the same thing.

All I can suggest is to get a quote elsewhere.

You can at least budget your money once you get a genuine exchange rate.

How safe are money transfers between Switzerland and the UK?

Not all companies have the same level of regulation or customer protection in place.

My advice would be to choose a company that is regulated by either the Swiss Financial Market Supervisory Authority (FINMA) or the UK’s Financial Conduct Authority (FCA).

You will find that Swiss banks will be regulated by FINMA, whereas most of the leading money transfer companies are regulated in the UK by the Financial Conduct Authority.

Both banks and fully regulated companies will verify customers to protect against fraud and money laundering.

It’s a sign you are dealing with a reputable company.

They are also required to keep your funds segregated in a safeguarded client account – which is kept separate from any company funds.

To find out if a money transfer company is Authorised, enter the company’s name in the FCA register.

Quick Summary

- You can use a bank or money transfer specialist to transfer money from Switzerland to a UK bank account.

- It should take 2-3 days for your money to arrive in the UK.

- There are two types of charges: fees and exchange rates.

- In terms of security, a regulated company will safeguard all client money.

- The larger your transfer, the more that costs and timing matter.

Who are we?

Key Currency is a leading money transfer specialist.

We provide a trusted and helpful alternative to using a bank for your international transfers.

The cost of our service is included in the exchange rate we quote.

It keeps things simple – you don’t need to factor in an assortment of fees.

One thing that sets us apart from the banks and online-only apps is we don’t push you onto a system and make you do everything yourself.

All our customers are assigned an account manager (a human being), who will assist them from start to finish.

Our account managers can also discuss target rates and technical levels to optimise the timing of your transfer.

We will work with you to get the best rates, avoid losses and reduce costs.

As a company, we are open and transparent.

The names, faces, and backgrounds of our people are shown on our website.

We have attained a 5-Star “Excellent” customer rating on the review website Trustpilot; which is the highest rating available.

We’re committed to providing a value-for-money service of the highest integrity and safety.

Key Currency Ltd is an FCA-regulated Authorised Payment Institution (No. 753989), and as such, all money transfers are conducted through safeguarded client accounts.

To make a no-obligation enquiry, please request a quote below.

Further Guidance & Tools

Information for the reverse transfer: Transfer Money to Switzerland

See the Live Rate: Pound to Swiss Franc Converter